Maximize Points: Credit Score Impact on Card Applications

On March 28, 2026 by pubmanMaximize Points: Credit Score Impact on Card Applications

Understanding the intricate relationship between your credit profile and financial opportunities is paramount for smart financial decisions. Specifically, the credit score impact on credit card applications is a fundamental aspect that determines not just whether you’re approved, but also the terms you receive, including interest rates, credit limits, and critically, access to the most lucrative rewards programs. Your credit score, essentially a numerical representation of your creditworthiness, serves as a primary signal to lenders about your reliability as a borrower, directly influencing their decision-making process.

How Does Your Credit Score Influence Credit Card Approval?

What is the direct link between credit scores and application outcomes?

When you submit a credit card application, lenders immediately turn to your credit score as a key indicator of risk. A high credit score signals financial responsibility and a history of on-time payments, making you an attractive candidate. Conversely, a lower score suggests a higher risk of default, often leading to application rejections or less favorable terms. This initial assessment is primarily driven by standardized scoring models like FICO Score and VantageScore, which distill your entire credit history into a three-digit number.

For example, an applicant with an excellent FICO Score (typically 750-850) is highly likely to be approved for premium credit cards offering exceptional benefits, such as significant sign-up bonuses, high cash back rates, or extensive travel perks. These cards are designed for low-risk borrowers who consistently manage their credit well. The application process for these individuals is often smooth, with quick approvals reflecting the lender’s confidence in their ability to repay.

On the other hand, individuals with fair or poor credit scores (below 670) will find their options significantly limited. They might be approved only for secured credit cards, which require a cash deposit, or credit-builder cards with higher annual fees and interest rates. The aim for these applicants is typically not immediate rewards maximization, but rather building or rebuilding a positive credit history, which is a crucial first step towards future rewards opportunities.

How do credit scores impact interest rates and credit limits?

The influence of your credit score extends far beyond a simple “yes” or “no” on an application. It directly impacts the financial terms of the card you are offered. A superior credit score can unlock access to the lowest Annual Percentage Rates (APRs), translating into lower interest payments if you carry a balance. For those focused on smart shopping, this means more of your money goes towards purchases, not interest.

Moreover, your credit limit is heavily determined by your creditworthiness. A high credit score often results in a higher initial credit limit, providing greater purchasing power and, importantly, a lower credit utilization ratio if you maintain your spending. A lower utilization ratio is beneficial for your credit score, creating a positive feedback loop that supports future financial goals. Conversely, a low credit score typically leads to minimal credit limits, which can quickly lead to high utilization if not managed carefully, potentially hindering further credit growth.

Therefore, optimizing your credit score before applying for new credit is a strategic move, allowing you to secure not only approval but also the most advantageous terms. This proactive approach is fundamental to maximizing the benefits of credit cards, whether it’s for travel rewards, cash back, or business expenses.

What are credit score ranges and their application implications?

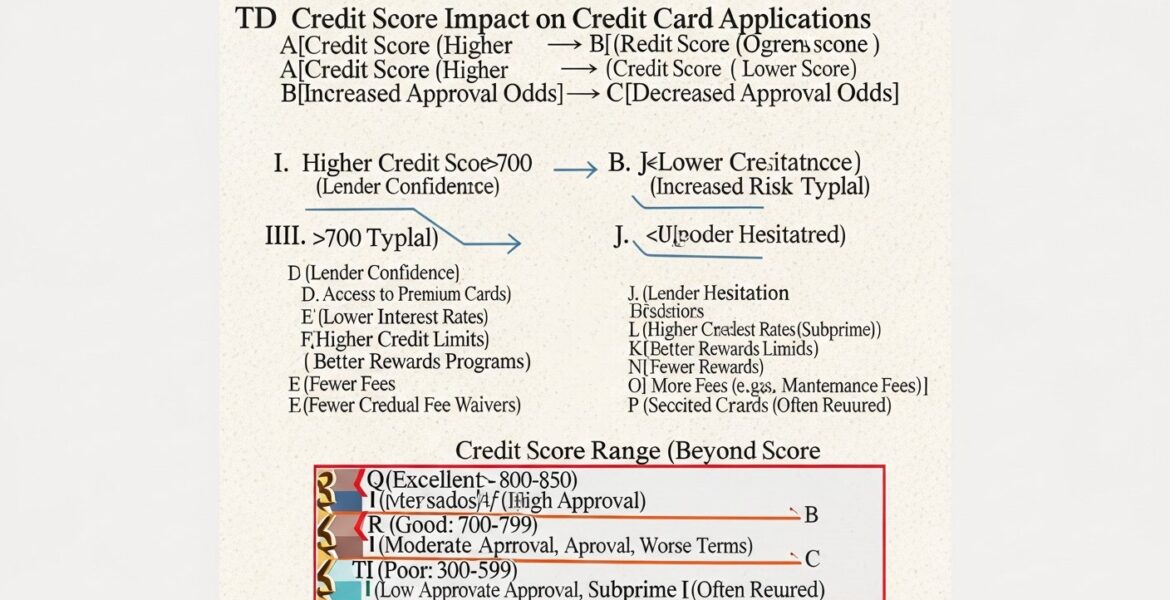

Credit scores are categorized into different ranges, each indicating a specific level of creditworthiness and consequently, distinct implications for your credit card applications. Familiarizing yourself with these ranges is crucial for setting realistic expectations and strategizing your card applications for maximum benefit.

| Credit Score Range | Typical FICO/VantageScore | Approval Odds | Typical APR Range | Credit Limit Potential | Accessible Card Types | Rewards Potential |

|---|---|---|---|---|---|---|

| Excellent | 750-850 | Very High | Lowest (e.g., 14-18%) | Exceptional (e.g., $10,000+) | Premium Travel/Cash Back, Luxury | Highest (Elite benefits, large bonuses) |

| Good | 670-749 | Strong | Competitive (e.g., 18-22%) | Good (e.g., $3,000-$10,000) | Standard Unsecured, Mid-Tier Rewards | Solid (Competitive cash back, travel points) |

| Fair | 580-669 | Moderate | Higher (e.g., 23-28%) | Lower (e.g., $500-$3,000) | Secured, Credit-Builder, Limited Unsecured | Limited (Basic cash back, few perks) |

| Poor | <580 | Very Low | Highest (e.g., 29%+) | Very Low (e.g., $200-$500) | Secured, Credit-Builder Loans | Minimal to None (Focus on rebuilding) |

How does excellent credit (750-850) unlock premium rewards?

Individuals boasting an excellent credit score are at the pinnacle of creditworthiness. Lenders view them as highly reliable borrowers, practically guaranteeing approval for almost any credit card product. This score range unlocks doors to exclusive benefits, including premium travel rewards cards like the Chase Sapphire Preferred or American Express Platinum, offering substantial sign-up bonuses worth hundreds or even thousands of dollars in travel, high earning rates on spending categories, and luxurious perks such as airport lounge access, travel insurance, and statement credits. Interest rates for these cardholders are typically the lowest available, and credit limits are often among the highest, providing significant flexibility for substantial purchases and maintaining low utilization.

What competitive offers are accessible with good credit (670-749)?

A good credit score positions you well for a broad spectrum of unsecured credit cards. While not as exclusive as the “excellent” tier, this range still qualifies you for cards with competitive interest rates and solid rewards programs. You can expect to be approved for popular cash back cards, entry-level travel rewards cards, and many 0% APR introductory offers. Cards like the Capital One Quicksilver or Discover it Cash Back are often within reach, providing valuable benefits without demanding a perfect credit history. Credit limits will be respectable, allowing for responsible spending and credit building.

How can fair credit (580-669) be a building block for better cards?

With a fair credit score, your options become more limited, but opportunities still exist for strategic credit building. You might qualify for unsecured cards specifically designed for those with average credit, though these often come with higher interest rates and lower credit limits. More commonly, secured credit cards are excellent tools in this range. A secured card, such as the Capital One Platinum Secured Credit Card, requires a cash deposit that often acts as your credit limit, mitigating risk for the issuer while allowing you to demonstrate responsible credit behavior. The focus here is on consistent on-time payments to gradually improve your score, paving the way for better cards in the future.

What are the options for poor credit (<580) like secured and credit-builder cards?

For those with a poor credit score, the immediate goal is credit repair and establishment rather than rewards maximization. Approval for traditional unsecured credit cards is very challenging. Options are primarily restricted to secured credit cards, where the deposit acts as collateral, or credit-builder loans, which are small installment loans designed to help establish a positive payment history. Interest rates on any available credit will be very high, and credit limits minimal. The objective in this range is to diligently make all payments on time and keep credit utilization extremely low to build a positive credit foundation.

What Specific Credit Score Factors Matter Most for Card Applications?

Lenders meticulously evaluate several key factors within your credit report to arrive at your credit score, each playing a significant role in their decision regarding credit card applications. Understanding these components allows you to prioritize efforts in building a robust credit profile.

| Credit Score Factor | Approximate FICO Weight | Impact on Credit Card Applications |

|---|---|---|

| Payment History | 35% | Crucial: Demonstrates reliability. Missed payments severely hurt approval chances and lead to higher APRs. Consistent on-time payments signal low risk. |

| Credit Utilization | 30% | Significant: High utilization (above 30%) signals financial strain, making lenders hesitant. Lower utilization (under 10%) indicates responsible management. |

| Length of Credit History | 15% | Important: A longer history shows sustained responsible behavior, increasing lender confidence. Shorter histories can imply less proven reliability. |

| New Credit | 10% | Moderate: Too many recent hard inquiries or new accounts can signal risk, especially for premium cards. Occasional new credit is fine. |

| Credit Mix | 10% | Lesser but Present: A healthy mix of revolving (credit cards) and installment (loans) credit demonstrates versatility in managing different credit types. |

Why is payment history the foundation of trust for credit card applications?

Payment history is, without a doubt, the most critical factor, typically accounting for about 35% of your FICO Score. Lenders want to see a consistent track record of on-time payments. Every single late payment, especially those 30 days or more overdue, is a red flag that significantly diminishes your creditworthiness. A spotless payment history reassures card issuers that you are a reliable borrower, making you a prime candidate for the best credit card offers and rewards programs. Conversely, even a few missed payments can drastically lower your score, leading to rejections or significantly worse terms on future credit card applications.

How does credit utilization impact credit card applications?

Representing roughly 30% of your FICO Score, credit utilization is the amount of credit you’re using compared to your total available credit. For instance, if you have a $10,000 credit limit and use $3,000, your utilization is 30%. Financial experts widely recommend keeping your overall credit utilization below 30% – and ideally even lower, like under 10% – to signal responsible credit management. High utilization rates suggest you might be over-reliant on credit or facing financial difficulties, which makes lenders wary of extending more credit through new card applications. Keeping utilization low not only boosts your score but also makes you more attractive to premium card issuers.

Why does the length of credit history matter for credit card applications?

The age of your credit accounts, accounting for around 15% of your FICO Score, reflects your experience as a borrower. Lenders generally prefer to see a longer credit history, especially with well-maintained accounts, as it provides a more comprehensive picture of your financial behavior over time. The longer your oldest account, and the higher the average age of all your accounts, the better. Closing old accounts, particularly those with a long, positive payment history, can inadvertently shorten your credit history and negatively impact your score, potentially hindering future credit card application success.

How do new credit and credit mix affect strategic borrowing?

New credit and credit mix each contribute about 10% to your FICO Score. Applying for new credit triggers a “hard inquiry” on your credit report, which can slightly and temporarily lower your score. While a single inquiry usually isn’t detrimental, numerous applications in a short period can signal financial distress to lenders, making them hesitant to approve additional credit. Similarly, a healthy credit mix – having both revolving credit (like credit cards) and installment credit (like auto loans or mortgages) – demonstrates your ability to manage different types of debt responsibly. While not as impactful as payment history or utilization, a diverse credit portfolio can subtly bolster your credit profile for credit card applications.

How can you optimize your credit profile before applying for new cards?

Taking proactive steps to enhance your credit profile before submitting credit card applications can significantly improve your approval odds, secure better terms, and ultimately lead to greater rewards. This preparatory phase is a crucial component of smart shopping and credit card rewards mastery.

What are actionable steps to boost your credit score?

- Pay Bills On Time, Every Time: This is non-negotiable. Set up automatic payments or reminders to ensure you never miss a due date. Payment history is the most impactful factor.

- Keep Credit Utilization Low: Aim to keep your credit card balances well below 30% of your total available credit. Paying down balances aggressively, especially before your statement closes, can yield significant improvements.

- Avoid Opening Too Many New Accounts: While building a diverse credit mix is good, opening several new credit card accounts in a short period can trigger multiple hard inquiries and lower your average account age, negatively impacting your score.

- Don’t Close Old, Paid-Off Accounts: Keeping old accounts open, even if unused, lengthens your credit history and contributes positively to your score and utilization ratio (as it adds to your total available credit).

- Address Derogatory Marks: If you have collections, charge-offs, or bankruptcies on your report, explore options like pay-for-delete (for collections) or debt management plans to mitigate their impact.

What should you look for when checking your credit report?

Regularly reviewing your credit report from all three major bureaus (Experian, Equifax, and TransUnion) is a critical step. You’re entitled to a free report from each bureau annually via AnnualCreditReport.com. When reviewing, pay close attention to:

- Accuracy of Personal Information: Ensure your name, address, and Social Security number are correct.

- Account Status: Verify that all accounts listed are yours and that their payment status (e.g., “paid as agreed,” “late,” “charged off”) is accurate.

- Credit Limits and Balances: Confirm that your reported credit limits and current balances are correct, as these directly impact your utilization ratio.

- Inquiries: Check for any unauthorized hard inquiries, which could indicate identity theft.

- Derogatory Marks: Look for any collections, bankruptcies, or foreclosures and ensure their reporting is accurate and within the legal timeframe.

If you find any inaccuracies or errors, dispute them immediately with the credit bureau and the creditor. Correcting errors can sometimes lead to a significant boost in your credit score, making a considerable difference in your credit card application prospects.

What common mistakes should you avoid before applying for a credit card?

Before you hit ‘submit’ on that credit card application, be mindful of common pitfalls that could jeopardize your chances or lead to less favorable terms:

- Applying for Too Many Cards Simultaneously: Each application results in a hard inquiry, which can slightly lower your score. A flurry of inquiries can signal desperation to lenders.

- Not Checking Your Credit Score/Report First: Going into an application blind is risky. You might apply for a premium card you won’t qualify for, resulting in a wasted hard inquiry.

- Closing Old Accounts to ‘Clean Up’ Your Report: This can backfire by shortening your credit history and reducing your total available credit, which in turn increases your utilization.

- Ignoring Small Balances: Even a small balance can carry interest and contribute to utilization if not paid off in full.

- Assuming All Credit Scores are the Same: There are many different scoring models (FICO, VantageScore), and scores can vary slightly between bureaus. Understand that the score you see might not be the exact one a specific lender uses.

Can You Get a Rewards Card with a Fair or Poor Credit Score?

While the most sought-after premium rewards cards typically require excellent credit, the landscape of credit card offerings has evolved, providing pathways to rewards even for those with fair or poor credit scores. However, the type and extent of rewards will differ significantly, and the primary focus should still be on credit improvement.

For individuals with fair credit (580-669), you might find entry-level unsecured rewards cards that offer modest cash back or points on all purchases. These cards often have lower credit limits, potentially higher APRs, and sometimes an annual fee. Examples might include cards that offer 1% cash back on everything. The key here is that while the rewards aren’t as lucrative as those for excellent credit, they still provide an incentive for responsible spending and on-time payments, which concurrently builds your credit profile. The rewards act as a bonus while you’re focused on graduating to better cards.

If your credit score falls into the poor category (below 580), direct access to traditional rewards cards is almost non-existent. However, you can still strategically work towards rewards. The path typically involves starting with a secured credit card or a credit-builder loan. While these usually don’t offer direct rewards, successfully managing them will improve your credit score over time. Some secured cards might offer minimal cash back, but their main purpose is to help you establish a positive payment history. Once your score moves into the “fair” or “good” range, you can then apply for cards with more substantial rewards programs.

The journey to maximizing rewards with less-than-perfect credit is a marathon, not a sprint. It involves using credit strategically, consistently making payments on time, and keeping utilization low. Each successful step builds your credit score, gradually unlocking access to better cards and more attractive rewards.

What is the role of your credit score in maximizing rewards and smart shopping?

At the core of “Maximizing Rewards & Smart Shopping” lies a healthy credit score. Your creditworthiness isn’t just a requirement for approval; it’s the gateway to unlocking the full potential of credit cards as powerful financial tools. Without a strong credit profile, the most lucrative offers simply remain out of reach, limiting your ability to earn substantial cash back, travel points, or exclusive perks.

Consider the impact: an excellent credit score allows you to qualify for premium travel cards that offer massive sign-up bonuses, often worth $500 to $1,000+ in travel. These cards come with high earning rates on everyday spending categories (like 3x points on dining or travel), extensive travel protections, and concierge services. For a smart shopper, these benefits translate directly into reduced travel costs, free flights, or significant cash back savings on all purchases. A high credit limit also means you can put more spending on a rewards card without negatively impacting your credit utilization, further amplifying your rewards potential.

Furthermore, a strong credit score means you qualify for cards with lower or even 0% introductory APRs on purchases and balance transfers. This allows you to finance large purchases interest-free for an extended period, or consolidate high-interest debt, saving you money that can then be redirected towards investments or further smart shopping opportunities. Access to low-interest rates also means that if you occasionally carry a balance, the cost is minimal, preserving your financial flexibility and keeping more money in your pocket.

Conversely, a low credit score forces you into cards with high interest rates, low limits, and often no rewards. This actively works against the principle of smart shopping, as any potential savings from a good deal are quickly eaten up by interest charges or annual fees. Therefore, understanding and actively managing the influence of credit scores on credit card decisions is not merely about getting approved; it’s about optimizing your financial future and truly mastering the art of maximizing rewards.

For more insights into leveraging your credit for optimal benefits, explore our comprehensive guide on Credit Card Rewards Mastery.

Frequently Asked Questions (FAQ)

Navigating the complexities of credit scores and credit card applications often brings forth several common questions. Here are answers to some of the most frequently asked:

Q: How often should I check my credit score before applying for a card?

A: It’s wise to check your credit score a few months before you plan to apply for a new credit card. This gives you time to address any issues or implement strategies to boost your score. Many credit card issuers and financial services offer free credit scores monthly, so regular monitoring is generally beneficial.

Q: Does applying for multiple cards hurt my score?

A: Yes, applying for multiple cards in a short period can temporarily hurt your score. Each application typically results in a “hard inquiry” on your credit report, which can slightly lower your score for a few months. A few inquiries aren’t usually a major issue, but many in a short timeframe can signal higher risk to lenders.

Q: Is it better to have a FICO Score or VantageScore?

A: Both FICO Score and VantageScore are widely used, but FICO is generally considered the industry standard, with about 90% of top lenders using it for credit decisions. While VantageScore provides a good general indication of your credit health, focusing on your FICO Score and the factors that influence it will likely be more directly relevant to credit card application outcomes.

Q: How long does it take for my credit score to improve after paying off debt?

A: The impact of paying off debt can be seen relatively quickly, often within one to three months, especially if it significantly lowers your credit utilization. However, building a substantially higher score through consistent positive behavior is a longer-term process, typically taking six months to a year or more for significant increases.

Q: Will closing an old credit card account affect my credit score?

A: Yes, closing an old credit card account can negatively affect your credit score. It can shorten your average length of credit history and reduce your total available credit, which in turn could increase your credit utilization ratio if you have balances on other cards. It’s generally advisable to keep old, well-managed accounts open, even if you don’t use them frequently.

Sources & References

- MyFICO: What’s In Your FICO Score?

- Consumer Financial Protection Bureau (CFPB): Credit Reports and Scores

- Experian: What Is a Good Credit Score?

- AnnualCreditReport.com

- TransUnion: What are the credit score factors that influence it?

About the Author

Priya Devi, Smart Shopper & Rewards Expert — I love uncovering the best deals and loyalty strategies to make your shopping more rewarding and your wallet happier. With a background as an E-commerce Loyalty Consultant and Consumer Behavior Analyst, I’m passionate about empowering consumers to make informed choices that benefit their finances.

Reviewed by Julian Thorne, Senior Editor, Loyalty & Consumer Engagement — Last reviewed: March 27, 2026

Reviewed by Julian Thorne, Senior Editor, Loyalty & Consumer Engagement — Last reviewed: March 27, 2026